Sweden is the largest economic entity of the five Nordic countries. The Swedish people have a high degree of acceptance of online shopping and strong consumption power. Its market is expected to reach $13.729 billion by 2024.

Keen Chinese sellers are aware of the considerable prospect of Swedish e-commerce market at the first time. If they want to explore this new blue sea market in Sweden, they must first understand the VAT situation in Sweden.

Sweden's VAT Act was formed in 1969, has a long history of 54 years, this act is administered by the Swedish tax office Skatteverket.

Which enterprises need to register for Swedish VAT?

Similar to the rest of the EU, overseas companies providing taxable goods or services in Sweden may be required to register VAT locally and pay VAT. Common cases are:

1. As an importer, import goods to Sweden for sale;

2. Set up a warehouse in Sweden and sell the goods stored in Sweden to buyers;

3. Have no inventory in Sweden, sell goods remotely to Swedish buyers from other EU countries/territories, and remote sales exceed SEK 320,000 in the current year or the previous year (starting July 1, 2021, the EU remote sales threshold is adjusted to a uniform €10,000), and the sales platform/EU enterprise does not declare using the OSS unified system.

4, you can voluntarily register for Swedish VAT. First, you do not need to pay attention to the remote sales threshold. Second, some sellers are EU EORI+ Swedish vat tax number when customs clearance, import vat can be deducted in Sweden.

Note:

1) The threshold for distance selling in Sweden is 320,000 Swedish Kronor (about 34,000 Euros), and from 1 July 2021, the threshold for distance selling in the EU is adjusted to a uniform 10,000 euros.

When your remote sales in Sweden are less than SEK 320,000 (€10,000 from 1 July 2021), you will be subject to local VAT on the taxable sales at the rates applicable in your home country, and you will only have to pay tax in your home country (i.e., sell abroad);

When you exceed the 320,000 sales threshold (€10,000 starting on 1 July 2021), you will be charged Swedish VAT on VAT taxable sales at Swedish rates, rather than using your own country's rates.

The distance selling rule applies only to goods, not services, and it only comes into effect when a taxable person in one EU country sells and delivers goods to someone (that is, not a taxable business) in another EU country.

When do I need to register for Swedish VAT?

The VAT department must receive the application for the VAT number at least 14 days before the first taxable supply.

As one of the EU member states, Sweden abides by the EU VAT rules. The VAT regulation, published by the European Union, sets out the principles by which member states, including Sweden, will adopt a VAT system. In EU member states these rules take precedence over local ones, which makes VAT laws different across the EU.

VAT rate and reporting cycle in Sweden

Tax rate:

1. Standard Tax rate:

25%, which applies to most goods and services;

2. Tax rate reduction:

12%, applicable to some food, non-alcoholic beverages, hotel accommodation, catering services, etc.;

6%, applicable to books (including e-books), newspapers and periodicals;

3. Zero tax rate:

Applicable to community and international passenger transport, property rental/sale, etc.

Deadline for VAT declaration in Sweden:

The deadline for VAT declaration in Sweden varies according to the filing cycle.

Annual report

You must file and pay VAT at the same time you file your income tax return if all of the following conditions are met:

* Your reporting period covers the entire Swedish fiscal year

* You are not transacting within the EU.

* You need to submit an income tax return and a VAT return

If your reporting period is for the entire Swedish fiscal year, but you are not required to file an income tax return, or you have made transactions within the European Union, you must report and pay VAT no later than the 26th of the second month following your reporting period (December is the exception, the deadline is the 27th of the month).

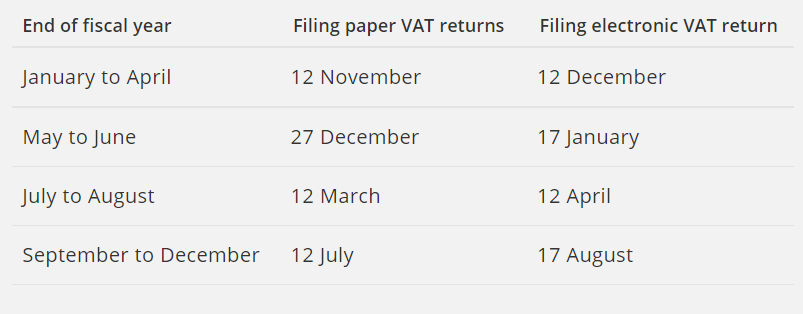

The deadline for you to report and pay VAT depends on when the Swedish fiscal year ends and whether you file your VAT and PAYE returns via an electronic service or by paper method. The following table lists all reporting and payment deadlines:

You must report and pay VAT on 12 May after the end of the Swedish fiscal year if all of the following conditions apply:

1) Your reporting period covers the entire Swedish fiscal year

2) You are not trading within the EU

3) You have to file an income tax return

If your company uses a representative to file a VAT return, your representative may have the right to suspend reporting and pay VAT until June 26.

Quarterly statement

VAT must be filed and paid by the 12th of the second month following the reporting period (except August, when the deadline is 17th).

For example:

VAT returns and payments for January to March must be received by May 12 at the latest.

Annual report

There are two possible VAT filing deadlines:

1) The sales volume of the current year does not exceed 40 million Swedish kronor, and the VAT refund deadline is not obtained in advance according to their own requirements. The deadline for declaration and tax payment is 12th of the second month after the end of the reporting period (except January and August, the deadline is 17th);

2) If the sales volume of the current year (Swedish fiscal year) exceeds 40 million Swedish kronor, the deadline for filing and paying tax is 26th of the next month after the end of the reporting period (except December, the deadline is 27th).