As competition in mainstream markets in Europe and the United States intensifies, emerging markets have become a new source of strength for cross-border e-commerce. Under the boom of "One Belt, One Road", the UAE is a rapidly rising economy in recent years. The UAE's customs and tax policies are important for cross-border sellers to exploit.

Recently, the UAE issued the latest policy concerning the customs clearance of freight forwarders and import VAT deduction.

For shipments to UAE, most Chinese sellers will use the double clearance tax model. This is mainly because UAE import compliance clearance requires local companies as IOR, product certification, import and export license and other issues.

Double clearance tax, is a more popular mode of transportation in recent years, as long as the freight forwarder to the shipper a specific total price, can solve a series of freight, insurance and related taxes and other problems. This way is relatively simple, and as the shipper (seller), after paying the freight can put the time and energy in other aspects, very time and effort saving.

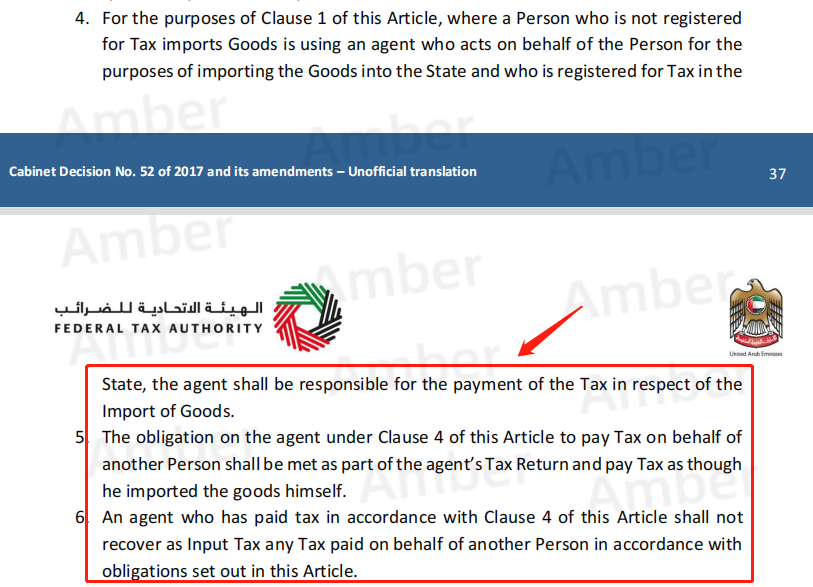

At the same time, we also know that when the forwarder's tax number is used for customs clearance declaration, usually the seller cannot deduct the VAT when declaring.

Recently, the UAE Federal Tax Authority (FTA) has issued a new policy allowing VAT taxes on imports to be deducted at the time of VAT declaration using a third-party agent tax number.

The implementation of this policy brings good news for importers who use forwarders for customs clearance.

Latest policy of UAE Tax Authority:

1) Even if you use the forwarder's tax number for customs clearance rather than your own tax number, you can also deduct it when declaring VAT;

2) The forwarder cannot deduct this part of import VAT paid by the seller.

The seller's preconditions for deducting this tax:

1. Declaration shall be made within 180 days after delivery of the goods, and only VAT charges related to the goods can be deducted.

2. Ensure that the tax number provided by the forwarder is valid, and require the forwarder to provide corresponding invoices and customs clearance documents as proof.

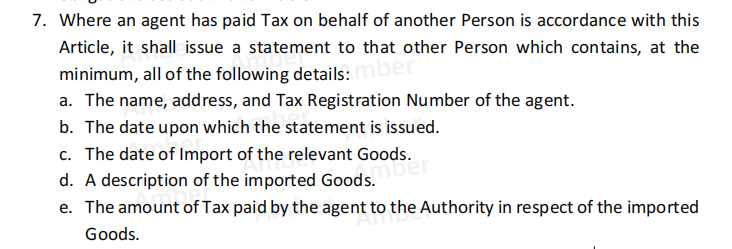

3. The forwarder issues a letter of declaration to the seller, which contains at least all the following details:

a. The agent's name, address and tax registration number;

b. The date on which the statement was issued;

c. Date of import of the relevant goods;

d. Description of imported goods;

e. Taxes paid by agents to authorities on imports.

In summary, the UAE Tax Authority has issued a new policy to allow importers who use the forwarder's tax number for customs clearance declaration to deduct the tax when declaring VAT.

The seller needs to negotiate relevant matters with the forwarder to ensure smooth customs clearance and declaration and avoid unnecessary disputes and losses.